北京考博斯特服装有限公司(110526××××)向日本出口一批服装。其中男长裤属于来料加工,货物位于加工贸易登记手册B75143217542第5项。装载货物的运输工具于2005年1月10日在天津新港发货。

从天津口岸运到日本的运费为USD450(1美元=112日元)。

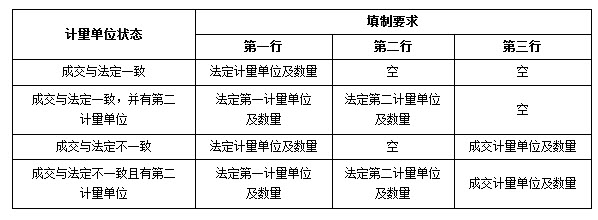

法定计量单位:条。(实际成交计量单位与法定计量位相同)

天津新港处于新港海关辖区。

SALES CONTRACT

CONTRACT NO:YB1046

DATE:Oct 29,2004 SELLERS:BEIJING KAOPOST GARMENTS CO.,LTD TEL: FAX:BUYERS:YUBST TEXTILES LTD TEL: FAX:This Contract is made by and between the Buyers and the Sellers;whereby the Buyers agree to buy and the Sellers agree to sell the under mentioned goods subject to the terms and conditions as stipulated herein after:

6.Packing:Standard export packing

7.Terms of shipment:By sea,Freight to be covered by the buyer,partial shipment is allowed,transhipment is not allowed

8.Port of Loading:Xingang,China

9.Port of Discharge:Kobe,Japan

10.Terms of Payment:payment by T/T

11.Time of Loading:Before Nov.15,2005

12.Special terms & conditions:

(1) Fabric and all accessories to be supplied by buyer,no commercial value.

(2) Allowance of quantity & amount will be 7% more or less.

THE SELLERS: THE BUYERS:

报关单中有20个已填(包括空填)栏目(标号A~T),请根据提供的单据指出其中填制错误。

参考答案:

A G K M Q

解析:

A项。该批货物的出境地为天津新港。 出口货物报关单的“出口口岸”栏应填报货物实际运出我国关境口岸海关的名称。因此,本栏应填报为“新港口岸”。

G项。在发票提示“TERMS OF PAYMENT BY T/T”,此栏应填报“T/T”。

K项。以FOB成交方式出口的,其出口货物报关单的运费栏不用填报。

M项。件数栏应填报有外包装的出口货物的实际件数,不能填货物的实际件数。在装箱单“PACKING LIST”显示为“31CTNS”,即31个纸箱。 因此本栏目应填报为“31”。

Q项。“数量及单位”栏应填报“法定计量单位”,即正确填报应为“1240条”。

[链接] 关于计量单位的填制要求如下表: