问题

单项选择题

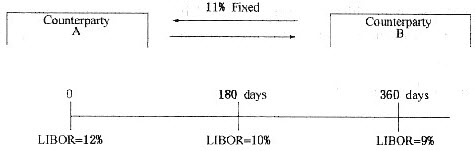

Consider a swap with a notional principal of $120 million.

Given the above diagrams, which of the following statements is TRUE At the end of 360 days :()

A. A pays B $0.6 million.

B. A pays B $6.6 million and B pays A $6 million.

C. A pays B $13.2 million and B pays A $12 million.

答案

参考答案:A

解析:

The variable rate to be used at the end of 360 days is set at the 180-day period (the arrears method). Therefore, the appropriate variable rate is 10 percent, the fixed rate is 11 percent, the time period is 180 days, and the interest payments are netted. The fixed-rate payer, counterparty A, pays according to:

(Swap Fixed Rate -LIBORt-1 ) (number of days/360 ) (Notional Principal).

In this case, we have(0.11 -0.1 )(180/360) ( $120 million) = $0.6 million.