Directions:

A. Study the following picture carefully and write an essay in no less than 160-200 words.

B. Your essay must be written clearly on ANSWER SHEET 2.

C. Your essay should meet the requirements below:

1) Describe the picture

2) interpret its meaning, and

3) give your comments.

参考答案:

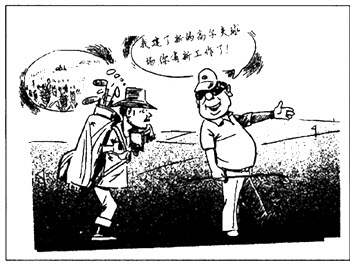

主题: Crying for land resources conservation

In recent years, more and more cultivable land of great worth has been excessively abused in the name of so-called economic benefits. Not surprisingly, a farmer in the picture is disappointed at the loss of his croplands, carrying a bundle of golf clubs for the player. Even worse, the miserable farmer is shocked when told that another large course is under way on the site of a cropland.

While it is true that golf courses must be signs of economic growths, it is equally true that land resources should be exploited in scientific and reasonable ways and that most course fields should be reserved for crop planting. Sure enough, the player in the picture may be building a golf course unwisely, regardless of the negative effects upon soil conservation of his reckless action, which leaves the farmer wondering where he could plant his crops.

This is a rather explosive situation for any farmers, whose lands are being tremendously misused. Unless the problem is conscientiously dealt with, the whole economy will surely break down because it must lose its solid basis of the agriculture.